1. Introduction

The Global Membranes Market encompasses the technology and industry surrounding thin, selective barriers used in separation processes across various sectors. Membranes function as filters, allowing certain components (like water) to pass through while rejecting others (like salts, particulates, or contaminants).

The market is driven by the urgent global necessity for clean water, sustainable industrial processes, and efficient resource recovery. Membrane technologies—including Reverse Osmosis (RO), Ultrafiltration (UF), Nanofiltration (NF), and Microfiltration (MF)—are now considered vital tools in addressing global water scarcity and meeting increasingly stringent environmental regulations.

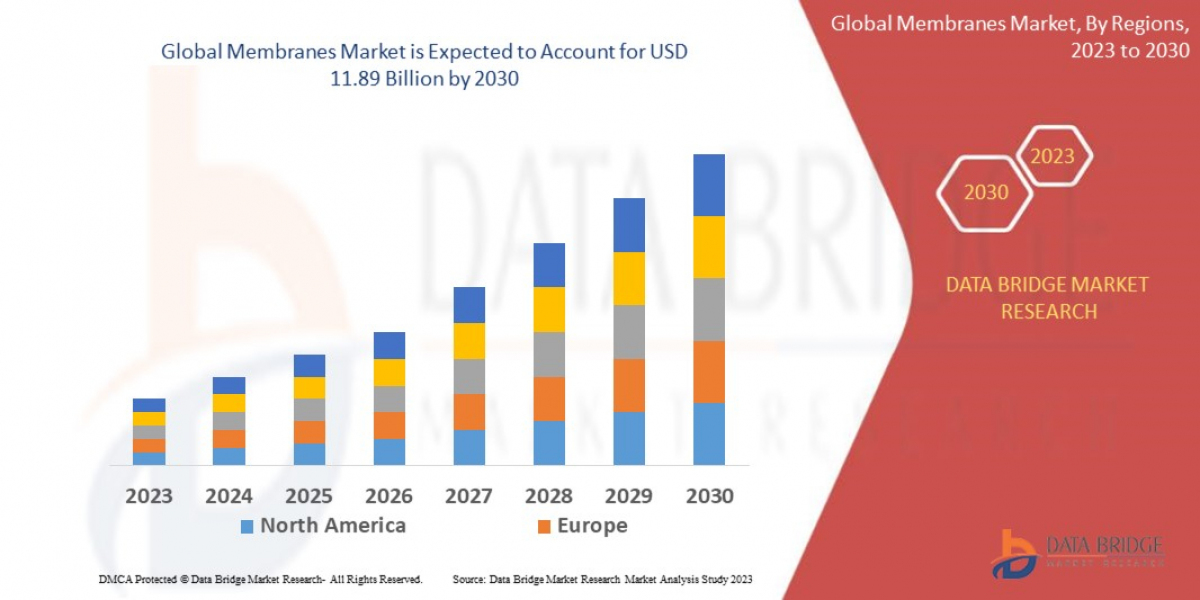

Data Bridge Market Research analyzes that the global membranes market, which was USD 7.55 billion in 2022, is expected to reach USD 11.89 billion by 2030, growing at a CAGR of 6.7% during the forecast period of 2023 to 2030.

2. Market Dynamics

2.1. Market Drivers

Escalating Global Water Scarcity: Rapid population growth, urbanization, and climate change are intensifying water stress, driving massive investment in desalination (especially RO) and municipal wastewater treatment/reuse projects.

Stringent Environmental Regulations: Governments worldwide are implementing stricter discharge standards for industrial and municipal wastewater, compelling industries (like chemical, food & beverage, and power) to adopt advanced membrane separation systems.

Technological Advancements: Continuous innovation in membrane materials (e.g., development of higher-flux, fouling-resistant, and energy-efficient membranes like Forward Osmosis or ceramic membranes) makes the technology more cost-effective and applicable across diverse industrial streams.

Growth in End-Use Sectors: High-purity separation needs in the Pharmaceutical and Biotechnology sectors (sterile filtration, drug concentration) and the Food & Beverage industry (juice clarification, dairy processing) are creating sustained demand.

2.2. Market Restraints & Challenges

High Upfront and Operating Costs: The initial capital investment required for installing membrane systems and the recurring energy costs (particularly for RO) can be a barrier, especially in emerging economies.

Membrane Fouling and Scaling: The deposition of organic matter, microorganisms, or inorganic salts on the membrane surface remains a critical operational challenge, leading to reduced performance, increased maintenance, and shorter membrane lifespan.

Concentrate Disposal: Handling and disposing of the concentrated brine (reject water), particularly from desalination plants, poses a significant environmental and logistical challenge.

3. Market Segmentation

The Global Membranes Market is primarily segmented across three key factors:

| Segmentation Category | Leading Segment (2024) | Key Alternative Segments |

| By Technology Type | Reverse Osmosis (RO) | Ultrafiltration (UF), Microfiltration (MF), Nanofiltration (NF), and Others (MBR, FO) |

| By Material Type | Polymeric Membranes | Ceramic Membranes, Metallic, and Others |

| By Application | Water & Wastewater Treatment | Industrial Processing, Food & Beverage, Pharmaceutical & Medical, Gas Separation, Energy |

Segment Insights:

Polymeric vs. Ceramic: Polymeric membranes hold the largest market share due to their cost-effectiveness, wide range of applicability (RO, UF, NF), and ease of fabrication. However, Ceramic membranes are the fastest-growing segment, favored for their superior durability, chemical/thermal resistance, and long lifespan in harsh industrial environments.

Reverse Osmosis (RO): Dominates the technology segment due to its widespread use in seawater and brackish water desalination and its ability to achieve the highest level of purification by removing monovalent ions.

4. Regional Insights

4.1. Asia-Pacific (APAC)

Market Position: Dominates the global market share (approx. 35-40%).

Drivers: Driven by rapid industrialization, massive population growth, and increasing government investments in water and wastewater infrastructure (especially in China, India, and Southeast Asia) to combat water pollution and meet rising demand.

4.2. North America

Market Position: Significant and mature market, often leading in innovation.

Drivers: Fueled by stringent federal and state regulations (e.g., on water discharge and reuse), high industrial adoption of membrane bioreactors (MBR), and strong demand from the pharmaceutical and food & beverage sectors.

4.3. Europe

Market Position: Mature market with strong growth, particularly in sustainability.

Drivers: Growth is primarily regulatory-driven, with a strong focus on circular economy initiatives, resource recovery, and high standards for potable water and industrial effluent quality.

https://www.databridgemarketresearch.com/reports/global-membranes-market

5. Competitive Landscape

The global membranes market is moderately fragmented, with a few large, diversified international players dominating the space alongside numerous specialized regional manufacturers. Competition is focused on R&D for new materials, anti-fouling technology, and system integration capability.

| Leading Market Players | Key Strategic Focus |

| DuPont (US) | Global leader in RO and NF membranes (FilmTec brand). Strong focus on water solutions. |

| Toray Industries, Inc. (Japan) | A major player across all membrane types (RO, NF, UF, MF, MBR). Known for continuous material innovation. |

| Kovalus Separation Solutions (Koch Industries) | Strong presence in industrial filtration and separation systems, offering UF, RO, and NF. |

| Veolia | A global environmental services giant, integrating membrane technology into large-scale water and wastewater utility projects. |

| LG Chem (South Korea) | A fast-growing player, particularly in the RO membrane segment for desalination. |

6. Future Outlook

The market is poised for strong expansion, guided by key trends:

Smart Membranes and IoT Integration: Future systems will increasingly integrate smart sensors and IoT (Internet of Things) for real-time performance monitoring, predictive maintenance, and optimized chemical cleaning to mitigate fouling.

Growth of Forward Osmosis (FO) and Membrane Bioreactors (MBR): FO and MBR technologies offer lower energy consumption and superior effluent quality, respectively, and are expected to see widespread adoption for challenging water sources and water reuse applications.

Sustainability and Resource Recovery: The shift will be less about waste treatment and more about Resource Recovery (recovering valuable resources like nutrients, metals, and energy) from waste streams using membrane technology.

Nanocomposite Membranes: Further breakthroughs in incorporating nanomaterials (e.g., carbon nanotubes, graphene oxide) will lead to next-generation membranes with ultra-high flux, superior selectivity, and excellent anti-fouling properties.

Browse More Reports:

Global Radiofrequency (RF) Micro needling Market

Global Radio Immunoassay (RIA) Reagents and Devices Market

Global Robotic Endoscopy Devices Market

Global GAN Epitaxial Wafers Market

Global Intranasal Antidepressant Market

Global Polybutadiene Market

Global Vestibular Neuronitis Treatment Market

Global Vitamin Deficiency Treatment Market

Global Automotive Bicycle Chain Market

Global Business Process Management (BPM) in Real Estate Market

Global Orthopaedic Imaging Equipment Market

Global Water Based Heliports Market

Global Medical Kits Market

Global Needle Destroyer Market

Global Makeup Tools Market

7. Conclusion

The Global Membranes Market is in a phase of dynamic expansion, fundamentally linked to the global priorities of water security and environmental sustainability. While high capital expenditure and membrane fouling remain challenges, continuous material and process innovation is steadily improving the cost-competitiveness and efficiency of membrane solutions.

The Asia-Pacific region will continue to be the primary engine of growth due to infrastructure investment, while mature markets like North America and Europe will drive demand for high-end, specialized applications and regulatory compliance. Membrane technology is cementing its position as the indispensable backbone for advanced fluid separation and purification across nearly every major industry.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com